Over the past few years, QuickBooks has gained so much popularity that these days majority of the small and medium businesses are using this accounting software. But after all it is just a software and like every other software, QuickBooks is also prone to some technical errors, one such error is QuickBooks error series 15XXX. In this technical article, we are going to focus on QuickBooks 15xxx (15000 series) errors which is a series of most common error codes that has been reported by many users. These error codes generally occur while downloading QuickBooks desktop or payroll updates. Incorrect configuration of Microsoft Internet Explorer might also cause these errors.

In order to protect the system and its content, the QuickBooks accounting software attempts to verify the digital signature of files that are downloaded via the program. If the QuickBooks accounting software can’t verify the digital signature of any file, then in that case the 15000 series error could be seen. If you want to know how to fix this bug, then stick to the article till the end, or you can also get in touch with our QuickBooks error support team via our toll-free number i.e. +1-888-510-9198. Our support team will ensure to provide you with the best possible support services in no time.

Simple process to Fix QuickBooks Payroll Error 15000 (15xxx) Series

The user can easily follow these troubleshooting methods in order to solve QuickBooks 15xxx series error. Also, he/she can take assistance from QuickBooks help team, in case the user is having some issues related to technical aspects.

Important: Before proceeding, remember that you have to install the latest version of Internet Explorer. (You can download it from Microsoft download center). If you already have latest IE version and still receiving the error then consult with your IT professional or go with Microsoft support.

Solution 5: Configure your firewall and anti-virus defender

The user is required to set-up your firewall program and anti-virus defender to check that your QuickBooks files are save and secure. If firewall is not configured and this can cause QuickBooks files to be corrupted when attempting to download updates or reinstalling any version into your system.

Solution 6: Download the Updates in Safe Mode

In case, the error still persists after follow the above steps then try to download the updates in safe mode.

First of all, the user is supposed to open your system in safe mode

After that, download the updates again

If it gets successful then restart your system in normal mode

Finally try to re-download the update

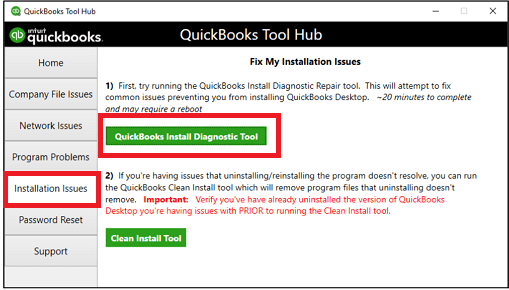

Solution 7: Run QuickBooks Install Diagnostic Tool

One can try performing the below set of steps to make use of the QuickBooks install diagnostic tool and eliminate the 15xxx series error. Let us have a look:

The very first step is to choose re-launch QuickBooks tool hub

Click on the installation issues tab in the tool hub

After that, choose the QuickBooks install diagnostic tool

The tool will start the fixation process

Reboot the system after the program fixes the installation and update issue

Rectifying QuickBooks error 15XXX series is not as difficult, as the users consider it to be. Carrying any of the above stated methods might help the QuickBooks users to get rid of the issue without any hassle. If by these methods, the error is not fixed then seek help from professionals or call the QuickBooks payroll Support service providers.

You need to dial +1-888-510-9198 and ask your query directly to our support executives. Our team of experts and certified professionals will help you in tackling the issue in the best possible way. Thus, do not hesitate in talking to our team, we will be happy to help you!

Frequently Asked Questions!

How do I fix error 15215 in QuickBooks?

To fix this error in QuickBooks, you can simply perform a windows restart in the selective startup mode. The steps involved in this process are as follows: 1. The very first step is to close QuickBooks desktop 2. And then, on the computer, select run 3. Now, in the run field, enter msconfig 4. And then, the system configuration utility will open 5. After that, you need to choose the selective startup and clear the load startup items checkbox 6. Followed by clicking on the save your changes tab 7. The last step is to reboot the system when asked

What is payroll update error in QuickBooks?

A bunch of errors in QuickBooks can occur due to various reasons, however, certain errors can be seen when updating the payroll in QuickBooks. If the download updates or shared location is mapped to a presently unavailable drive, then you can come across payroll update error in QuickBooks.

What is QuickBooks 15222 when updating QuickBooks desktop?

The error code 15222 occurs when the application is unable to establish a connection with the internet to download the update files, and this can happen due to various reasons like anti-spyware, anti-adware, anti-malware, etc.

Have you ever heard of SUI rate for basic, enhanced, or standard payroll? Well, SUI tax rates stand for State unemployment insurance. It provides employees who lost their data for different reasons with a short-term benefit. Moreover, when you mistakenly put-up state taxes or payroll items. QuickBooks incorrectly deducts unemployment from an employee’s paycheck. You state sets your SUI rate. And this rate is unique to every business. In case you are a new employer, your state will assign you a new employer rate until you file unemployment taxes for a certain period of time. Often when SUI rate changes, you will have to update it in payroll. This surely keeps your SUI tax liability accurate. It should be noted that the state unemployment insurance is only paid by the employer, unless the state requires employees to contribute.

In addition to that QuickBooks 2013 for windows requires a valid Intuit payroll subscription with recent upgrades being installed. You can further configure QuickBooks to accurately compute unemployment as long as the employee hasn’t used up all of the state unemployment insurance benefits. To learn further about SUI and to explore the process to change SUI, make sure to stick around this piece of writing carefully. Or you can further connect with our tech support team in case of any queries. Feel free to reach out to us at +1-888-510-9198, and we will answer all your queries immediately.

Facts Related to SUI Tax

These SUI rates are important for your large business and that is issues by a state.

SUI tax rate is not a part of payable tax & it is critical that a user enter their tax rate in their QB desktop software.

This tax is paid by the employer until and unless your state and employees contribute with each other.

SUI wage limit will be rationalized through the tax table as per rules according to which state you belong to. Remember one thing, this will not be modified by a manual.

In the beginning of a financial year, many states will already update SUI tax rate. In fact, others such as New Jersey, Vermont and Tennessee will update their SUI tax rate in the first quarter of a financial year.

QuickBooks Payroll software is used to manage your accounting in a well-planned way. With the help of this payroll, this brings our work less stress and reduces the workload by consuming less time. If you have any queries, then ask expert advice directly from our QuickBooks Consulting Service team.

Method that Describes SUI basic, Enhanced or Standard Payroll

Know what the facts about SUI tax rate are

All rates are exclusively unique for every new business & this can be issued by any state.

The rate is also not a part of an updated tax table. It’s critical that you enter the current rate in your QuickBooks Desktop.

If it is paid by an employer, it is unless that you’re in a state or want to contribute by the employees.

Steps to Change the SUI tax rates in Enhanced or Standard Payroll

Now we need to understand that points to change SUI tax rate in Enhanced Payroll & Standard payroll

First of all, choose an option of Lists. Then click to the Payroll item list.

After that, double-click on the SUI tax item, which is typically named: [state abbreviation] – unemployment company.

Then click on the next key button. Click on the company tax rates as yearly.

An account is also required to type correct rates as per quarterly.

Note: Remember one thing that if your device date is 7/1 & 1/1 that a user will now able to include the rate for a first quarter as for annually.

While to do so if you mention all correct rates or a user get an error message as Payroll Tax Rate Change Warning on your desktop screen. Now click the continue option. Thus, the user SUI rates will now be updated.

Now click on the next option and then give a one clicks to clear of all unnecessary items which are having no matter related to SUI tax.

After this, give a click to the next option and then click on the finish button, if troubling somewhere then asks expert guidance provided by QuickBooks Payroll Support team.

If you want to change or require you to make some modifications in Sui wage bases or sums that are reports to our workers. Set up a payroll report and standardized these numbers.

Here are some tips describing as that boost to change SUI tax rates and enhanced or standard payrolls as explained here: –

Firstly, select or click as reports & then click to an employees and payroll option.

After that, set the date to keep track as quarterly.

Now click to customize the accounting report and select the following details.

Date required for proper information.

Want the Source Name for that report.

Which Payroll Item you’re using.

Wage Bases of a payroll.

Total amount mentioned in the given payroll.

While to do so, click the filters option, in the above list, select the payroll items.

Now give one single click to the payroll item. Select the State unemployment item.

Now let us look at the total wages that are based upon the column and can increase the present rate.

At the end, users need to match all sums that you have calculated.

Hopefully, this article helped you to understand about SUI Tax Rates & how to change in basic, enhanced or standard payroll, if troubling somewhere or have any query then feel free to contact us at our QuickBooks support number through given toll-free number +1-888-510-9198. Thanks for visiting our page, if you want any additional services our Certified ProAdvisors team is available to help you with all accounting and bookkeeping solutions.

If you are facing errors while operating or accessing your payroll account? Then you’re at the right place where end users will get instant solutions provided by our Intuit certified Pro Advisors. No more wait, give us a call on our toll-free number +1-888-510-9198, and share your problems with our experienced professionals who have years of experience sorting out all accounting and quick booking solutions. Thus, our accessibility is round the clock. It’s too easy to connect our experts that are more qualified and highly knowledgeable in resolving all sorts of hindrances in real-time.

FAQs Related to SUI Rate in QuickBooks

What is the process to alter tax rates in QuickBooks?

To alter tax rates in QuickBooks, you can perform the below steps: 1. Open QuickBooks company page and choose reports from the menu 2. Choose item list 3. Every item that is stored in QuickBooks will be visible 4. Locate customize report in the top menu bar and click on the same 5. Press filter tab 6. Choose account after that, and select all liabilities from the drop-down box. 7. The sales tax list should be printer 8. Click on print and choose report from the list 9. When a new window appears, select your printer and press print tab

How do I change payroll settings in QuickBooks?

You can change the payroll settings in QuickBooks using the steps below: 1. Open QuickBooks desktop company file and sign in as QuickBooks admin 2. Choose edit, and go for preferences. 3. From menu choose payroll and employees 4. Go for preferences tab 5. Ensure that QuickBooks payroll features is set to full payroll

What is Sui Basic?

State unemployment insurance is a tax funded program by employers to give short term benefits to workers who have lost their job. This tax is needed by state and federal law. Unemployed workers receive these benefits on the condition that they are looking for new job.

For the past decade QuickBooks have changed the way accounting activities are performed. Now it is no longer a time taking and complicated task, and all thanks to this new age accounting software. All across the globe small and medium businesses are now making use of QuickBooks for accounting as well as payroll. It has made business operations much smoother by streamlining financial management system. In this article we have discussed about the complete procedure of QuickBooks Payroll Setup Checklist in Intuit Desktop Payroll & Online Payroll.

Even though QuickBooks Payroll comes with many benefits it is a bit complicated. Today, this path breaking software is being used on desktops, laptops, and even cloud and it also offers various amazing features suitable for various devices, as well as operating systems. If you are planning to setup desktop or online payroll account, QuickBooks Payroll might require certain information. Here is the checklist for the information that you would require during the set-up of the software. Apart from this, if you have any other query regarding the software or face any error you can directly call to Intuit QuickBooks help community. Or you can give us a call in our 24/7 QuickBooks payroll support number i.e. +1-888-510-9198 and our Intuit certified ProAdvisors who have years of experience will be ever ready to help you in this.

Setting up payroll will be a smoother process if you can collect the following information first:

Category

Type of information needed

Company

The frequency that employees are paid (weekly, every other week, twice a month, or monthly)

The date you plan to start using Payroll

The first pay period that you’ll run within QP

Compensation, Benefits, Contributions and Deductions

Types of compensation (hourly wages, salaries, commissions, vacations)

Sick and vacation time policies

Insurance benefits (health, dental, vision)

Retirement benefits offered (RSP)

Additional deductions that the employee wants withheld (for example, child support, repayments of employee advances or loans, life insurance)

Additions (bonuses, travel reimbursements, employee advances or loans and tips)

Tax Information

Federal tax business number (BN)

CRA Payroll number

T4 transmitter number

RQ payroll information

Employees

Employee names, addresses, and Social Insurance Numbers from your employees’ T4 forms

Employee withholdings from the employee’s TD1 form

Employee wages/salaries, additions, deductions, and company contributions

Sick and vacation time hours and monies accrued

Year-to-Date History (YTD)

You’ll need to enter year-to-date payroll information ONLY if you’ve started using QP after January 1 of the calendar year AND if you’ve already run payroll using another system at least once since January 1. (If you start using QuickBooks Payroll after January 1 but have not yet run a payroll this calendar year, you will have no year-to-date information to enter.)

Year-to-date information for each employee is available on the employee’s most recent pay stub from the previous system.

Copies of payroll liability cheques from the beginning of this calendar year to the date you started using QP

Note: once you run a payroll in QuickBooks Online, you’ll no longer be able to add or edit year-to-date information. Be sure to add all employees and payroll data prior to running payroll

QuickBooks payroll requires certain information for setting up in the QuickBooks desktop or even in QuickBooks online payroll account. Once the user completes the set up process, after that it is very easy to spot all the information form the previous payroll provider, or from the records, accountant, federal and state agencies, etc.

QuickBooks users have a plenty of options for payroll on QuickBooks desktop or even in cloud, and the user needs to make a wise decision of selecting the most appropriate out of many.

No doubt, QuickBooks desktop payroll, as well as QuickBooks online payroll has a large customer base, and thus it is ensured by the developers to offer a wide range of options to suit the needs of every user. The varied options are very much confusing for the user, and that is why our team ensures to help the users in opting for the best option that suits their requirements.

The Desktop Payroll version is one of the best and is being used by many entrepreneurs all across the globe. Though it is used by many users, there are a few who like their data on the desktop as they don’t like changes. Many users resist change, but it can bring many perks.

Some option for Desktop that runs on the desktop versions:-

No QuickBooks payroll tax form filing.

QB payroll tax filing and good job costing and the ability for yourself.

QuickBooks Desktop Enter the Payroll hours and amount.

QB Desktop features of Enhanced.

QuickBooks desktop Payroll service is pretty easy to use and that’s why bookkeepers, accountants, business owners and even individuals can make use it. However, for the desktop version it charges per cheque, but for the online versions the direct deposit is free of cost. For any further information regarding the setup of the desktop version reach us out via our 24/7 toll-free .I.E. +1-888-510-9198.

QuickBooks Online is another version that is widely used and it is within the QuickBooks Online Payroll along with Intuit Online Payroll. You have to integrate into QuickBooks so that it runs from there. This is a very important step to do, so as to make sure that the tax rates as well as the previous payrolls are recorded properly. This is because it isn’t easy to change in the online version without an adjustment as it can be done in the Desktop version.

This one is a very good option for the QB Online Payroll users who have QuickBooks Online or who have not used QuickBooks ever in their life.

QuickBooksOnline Payroll

Just like the Intuit Online Payroll, QuickBooks Accountant version is a new age product that is packed with many amazing features and have brought significant changes in the organizations operations. The Intuit QuickBooks Online Payroll doesn’t charge direct deposit fees but it charges $2.00 per person every month if there is one client.

But what is great about it is that the monthly fee and per person charge drops when you get more than one clients. You make a great profit as the charge drops to $0.50 per employee and with more than one client.

A great thing is that clients have their own logins and passwords so that they can handle their own payroll. And once they set up the QuickBooks, Intuit Online Payroll, the need to worry about it doesn’t arise, except for the taxes. If you want to know more about Intuit Online Payroll you can consult with our Intuit Certified ProAdvisors.

We have been in the industry for a long time now, and this has helped us in learning a lot about the software. And that’s how we render quality, as well as quick support service to our customers. We are available 24/7 through our toll-free customer care number to listen and help out our clients. So, why wait, dial our QuickBooks support number+1-888-510-9198 and get an instant solution to any QB related problem.